January 2025 Update

January 22, 2025 By Ilona

2024 market saw a few distinct changes. Higher inventory and massive price reductions. We are already starting to see a small change in pricing – roughly 5 – 7% depending on location. If inventory keeps rising, we could see the pricing change go up.

Here’s how December Year over Year looks:

|

December 2024 |

December 2025 |

|

| Active – 585 | Active – 434 | *Single Family |

| U/C – 244 | U/C – 235 | *All Classes |

| Absorption Rate – 6.59 | Absorption Rate – 4.89 |

As you can see inventory is up 35%.

Yet the number of properties under contract is about the same. While that number has not gone down, what happens when you have more homes for sale and the same or fewer buyers? Law of supply and demand is in play. That is why the absorption rate (months of inventory) has gone up so much.

The statistics are telling us the slow down will continue this year. With mortgage rates higher and mortgage applications at their lowest levels ever, we could see a double-digit drop in pricing this year. I’ll be watching!

November OBX Update

November 13, 2024 By Ilona

November Market Update

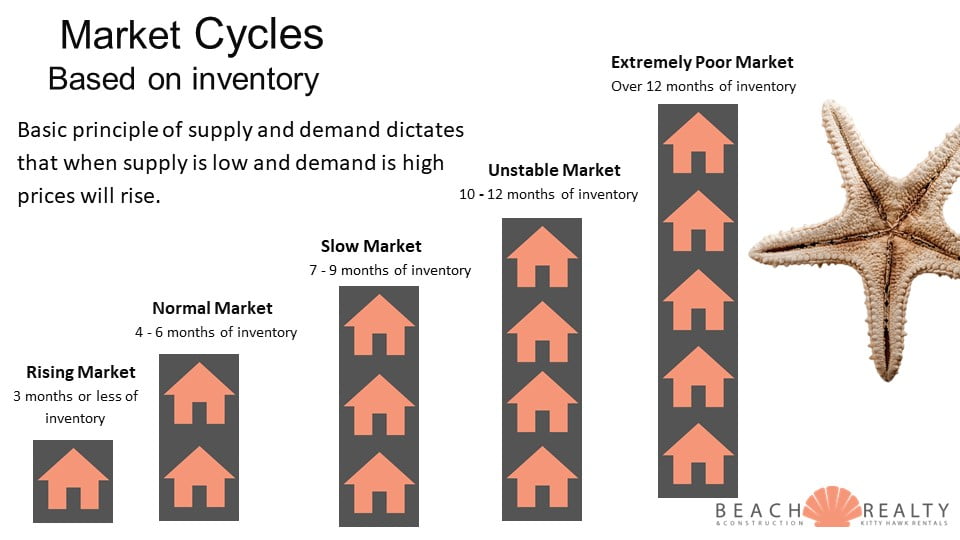

Still a bit of a holding pattern in what supply and demand would still deem a “Normal Market”.

Normal is an inventory level of 4 to 6 months. We are right on the cusp of moving to a “Slow Market” where the advantage shifts over to the buyers in the market.

| January 2024 | November 2024 | |

| Active Inventory All | 870 | 1187 |

| Active Inventory Homes | 424 | 595 |

| Under Contract | 24% | 19.50% |

| Absorption Rate | 5.4 | 6.7 |

| SF Absorption Rate | 4.3 | 5.3 |

| Price Reductions/Month | 171 | 271 |

If you would like a more specific analysis for your real estate goals, give me a call!

July OBX Market Stats

August 2, 2024 By Ilona

While there isn’t much change to report this month, I predict by October/November there will be more inventory and the beginning of a quantifiable shift in pricing. You know I’ll keep you posted! To see the full effect of the logarithmic path, I’m comparing January 2024 to July 2024.

| Jan 2024 | Jul 2024 | |

| Months of Inventory | 4.8 | 5.9 |

| Active Homes | 492 | 700 |

| % Under Contract | 24% | 21% |

| Price Changes/Month | 171 | 232 |

2024 Second Half of the Year Weird Market Selling Strategy

June 26, 2024 By Ilona

As we approach the second half of the year, it’s important to notice the little shifts happening along the way. Remember, real estate markets don’t crash overnight. It happens slowly at first, then all of a sudden. We are in the slowly at first phase.

As we approach the second half of the year, it’s important to notice the little shifts happening along the way. Remember, real estate markets don’t crash overnight. It happens slowly at first, then all of a sudden. We are in the slowly at first phase.

Our market here gets insulated because it’s not a primary market. Being a discretionary sale and discretionary purchase for the majority of transactions, it provides a lag time from when we start to see primary markets destabilize.

If you are thinking about what to do with your OBX investment home, you need to look big picture. Consider first and foremost, just because you don’t HAVE to sell, does not automatically mean that keeping the home is in the best financial interest for your family. Always consult your financial adviser for guidance.

Let’s now take a look at the two options, sell or keep. Regardless of what you choose, this information will help you set up the best expectations for either choice.

Sell

- Good news! Prices are still at record highs. You have not missed the boat.

- However, pricing strategy must remain fluid. No longer set the price and then 3 months later look at it. If you want to maximize profit here, you must be the trend setter, not the follower.

- Inventory is rising – up 29% from this time last year

- Demand is dropping – down almost 10% from last year, and last year demand dropped 50% from 2022

- Price reductions are increasing – in May 368 new listings came on and 287 listings had a price reduction

- Must be negotiable – 66% of properties sold are below asking price.

- Affordability is still the number one concern for buyers

If you employ a listing strategy with this in mind, you will maximize your return and get the home sold in a reasonable amount of time.

Keep

- Remember how these cycles have worked over the years.

- Boom 1985/86 – fell apart early 90’s – stagnant until 2000.

- Boom again 2004/05 – fell apart 2008/09 stagnant until 2019/20.

- Boom 2021/22 – 2023 activity dropped by half, pricing is just starting to crack with price reductions and under asking price sales.

- If the pattern continues it could be stagnant again until 2035 or longer.

- Rising Insurance as well as other increasing vendor costs.

- be prepared for at least a 14% increase in dwelling policies and unknown yet for homeowners.

- Service providers are increasing costs: lawn care, pool/hot tub maintenance, linens, etc

- Return to pre-pandemic rental income.

- It starts with lower vacancy rates. 2024 is already seeing only 90% booking.

- Next will be set lower rates – discounts are already happening.

- If you stay, the cost to own will go up, with income to support going down.

- Prepare for capital improvements.

- Tightening insurance underwriting regulations are requiring updates to stay insured. Roof, water heater, etc

- Continued lack of demand for homes that have not been updated. Especially as inventory increases, you’ll need to have prime condition and updating to be chosen.

- Reality of a major storm this year or next. Let’s face it, no one likes to say it, but we haven’t had a hurricane since 2018. Generally, we see a 6 to 9 year pattern.

If you do decide to keep the home through the next cycle, let’s at least put together a plan to get your home updated and where to best spend the money. I also have a list of trusted vendors who can help you get things done.

Now that you have the big picture, let me know if I can be of any help as we navigate this next market shift.

May OBX Market Update

May 15, 2024 By Ilona

In a nutshell, the market here is changing…slowly…but surely. These types of cycle shifts don’t happen all at once. Fortunately, because I study the market every day, I can help you see it coming. After all, you can get out of the way of what you don’t see!

In a nutshell, the market here is changing…slowly…but surely. These types of cycle shifts don’t happen all at once. Fortunately, because I study the market every day, I can help you see it coming. After all, you can get out of the way of what you don’t see!

Here are the basics we are watching:

Inventory

Total Everything – up 27% since January (currently over 1,000 listings)

Homes, Single Family and Condos/Townhomes – up 24%

Activity

Absorption Rate has gone from 4.8 months to 5.5 months since January

This means it would take longer to sell the homes we currently have on the market. Once this goes over 6 months, we enter a Slow Market

Price

53.5% of homes are still selling within 0-30 days, of those…

97% of asking price is what they are selling for

67% of homes are now selling under asking price

Basic supply and demand economics tell us that when supply is inching up, demand is inching down that prices will start to waiver. How long will this current market last? We just have to keep watching. We are noticing more price reductions coming in and fewer multiple offers. This is an active situation. Stay tuned for next month’s report!

If you have thought about buying or selling, let me know so we can plan your strategy.

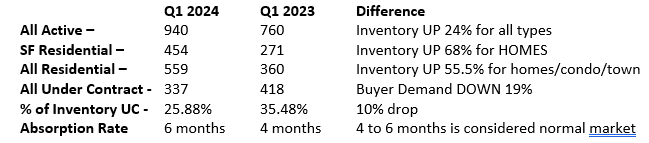

First Quarter 2024 Comparison to First Quarter 2023

April 5, 2024 By Ilona

What a difference a year makes! Long story short, there are some BIG moves that are happening. I’ve talked before about algorithmic decay. This chart here is exactly that! Little, by little, by little, then bang. That’s how markets change. Tale as old as time, song as old as rhyme, it’s almost as good as a crystal ball.

What a difference a year makes! Long story short, there are some BIG moves that are happening. I’ve talked before about algorithmic decay. This chart here is exactly that! Little, by little, by little, then bang. That’s how markets change. Tale as old as time, song as old as rhyme, it’s almost as good as a crystal ball.

Anyone saying the real estate market on the Outer Banks is not changing is just not paying attention.

But, look here, and you decide:

We are on the cusp of a price shift potentially starting this fall. Here are the facts about our market:

- Insurance costs are rising and coverage dropping

- Interest rates are not changing any time soon

- Rental income is back to pre-pandemic levels

If you are on the fence about selling your home, your window is closing before we start to see quantifiable price shifts. Call me today to discuss the best strategy for selling in today’s changing market.

How NOT to set the listing price of your home.

March 7, 2024 By Ilona

A lot of agents will do presentations on how they came up with a price for your home. It is a task that does require some skill. The challenge of course is getting the seller to agree to the pricing suggestions.

A lot of agents will do presentations on how they came up with a price for your home. It is a task that does require some skill. The challenge of course is getting the seller to agree to the pricing suggestions.

Many sellers come into the meeting with a general idea of what they want for the home, which is helpful. However, here are a few ideas on what NOT to do when you decide to sell your Outer Banks home in today’s market.

- Tax Assessment – Don’t confuse your county tax assessment with market value. Your tax assessment is for the purpose of assessing a tax amount to you for the purpose of revenue to the county. It doesn’t in any way suggest that’s what a buyer is willing to pay or a seller is willing to sell for. Most importantly the assessment on your home right now is 4 years old! On the Outer Banks they only re-assess every 8 years. Because it’s 4 years old, it also doesn’t take into consideration any improvements that have been done since the last assessment.

- Old Appraisal – Appraisals are only good for the day they are written. What? Yes, that’s correct. Considering that anything and everything could change tomorrow, an appraisal can only be valid for one day. If you have a year-old appraisal and want to base your price on some reflection of that, you might find yourself the highest bidder of your home. I mean I was a size 8 years ago, but that’s not exactly going in my dating profile for today!

- Old Sales in the area – All agents have heard it… “Well, my neighbor sold last year for $30,000 more.” Markets never stay the same. It’s an ever-changing environment, which is why consulting with a good agent who studies home prices every day is the best way to get closest to current market value.

- Recent Improvements – We’ve also all heard… “Well I have a new roof, HVAC and carpet. I want to ask $extra to cover those costs.” The fact that you’ve done these “maintenance” items is great. It shows you’ve taken care of the home. The problem is all houses need a roof, HVAC and carpet. In this market, that can make your home more saleable, not necessarily more valuable. Buyers expect the basic components to be in good condition already. What you can ask more for are upgrades. Changing vinyl to tile or carpet to hard wood, or laminate to granite are all upgrades.

- Basing the price on your needs – We would all love to get the seller the most money possible. That’s part of our job. However, we can only sell the home for the true market value. Just because you NEED to get $50,000 at closing doesn’t mean it’s going to happen. You have to consider all the current factors in your marketplace and if those point to a lower price, you needing that money will not cause a buyer to pay it if the value isn’t there. You may need to adjust your plans based on what’s realistically going to come out of the sale of your home. These are hard conversations, but a good agent will not be afraid to spell out the truth.

- Stuck on a previous market value –The last few years have been monumental. It was a fast- rising market and prices skyrocketed. Now we are in a more “normal” market. Prices aren’t rising or falling at a tangible rate just yet. Mostly because inventory is still too low. However, don’t get complacent. Markets ALWAYS cycle. What goes up, must come down. I predict this fall pricing will look differently than it does right now. So, pay attention to CURRENT trends and not what happened the last year or two.

- Focus only on Price – So often I hear, “I don’t have to sell, I’ll just wait if I have to sell at that price.” Selling a home is based on a LOT of decisions, not just the price for it. No one wakes up and turns to their spouse and says “Honey, the house is worth $X, we have to sell it.” Selling is based upon life changes, new needs, maintenance costs, jobs, marriages and so many more things that are related to the way we live our lives. It’s sometimes concerning when I see a seller refuse to sell based solely on the price. That means they are putting that dollar value above the benefits selling the home can bring to the family. Don’t let the emotional response to the price create a “wish I would have” moment.

Now that we’ve covered what NOT to do, if you need help pricing your Outer Banks home for a prime spot in our market today, certainly let me know how I can assist you!

OBX History Repeats Itself

January 8, 2024 By Ilona

History repeats itself. A saying I’m sure you’ve heard and said dozens of times. I might not yet be a half of a century old, but I’m old enough, and have been in this business long enough (27 years) to recognize a similar pattern. Let’s revisit the timeline of the Outer Banks real estate market from the year 2000.

History repeats itself. A saying I’m sure you’ve heard and said dozens of times. I might not yet be a half of a century old, but I’m old enough, and have been in this business long enough (27 years) to recognize a similar pattern. Let’s revisit the timeline of the Outer Banks real estate market from the year 2000.

Year/Sold Units Sold Average Price Sold

2000 n/a* $275,000 *I don’t have access to the # of sales that far back

2005 2104 $555,973

2008 1045 $427,718

2011 1333 $370,569

2014 1611 $370,351

2017 1995 $385,774

2019 1966 $400,592

2020 2614 $520,009

2021 2889 $668,994

2022 2096 $770,901

2023 1446 $746,351

Looking at the raw data above for single-family home sales, here’s what we see:

- Between 2000 and 2005, there was a building boom and a huge spike in demand due to the subprime loan accessibility.

- 2005 was the peak of that bull cycle – 2006 slowed, 2007 started looking quite ominous.

- 2008, there was a 50% drop in buyer demand or the number of homes sold.

- 2011 – 2014 was the lowest point, with a 32% overall drop in pricing.

- In the 8 years from 2011 to 2019, pricing stayed flat, only going up 5% overall.

- By 2019, buyer demand came within 7% of the peak number of sales in 2005.

- Right on schedule, 20 years from when the boom started in 2000, a new cycle started.

- Buyer demand shot up, and pricing came back to just under the 2005 peak.

- Notice now that in 2023, the first step to a declining market, just like in 2008, is a drop in buyer demand. An exact replica of a 50% drop in home sales from the peak in 2021.

- This time, the 2022 peak pricing was 39% higher than the peak pricing in 2005.

- If the market drops at 35%, pricing still hovers over $500,000.

Now, I know that is a lot to unpack. All of this data is telling me that the drop in home sales is a clear indication that we have reached the peak and are on the way back down and soon. The last peak was in 2005, and the crash is attributed to 2008. That 32% decline in pricing didn’t happen overnight. It was spread out over a few years.

So, what does all of this tell us?

- First, based on the last cycle, even after the crash, the average price still never went below $300,000.

- If the same holds true, pricing will return to $500,000 after this cycle, but you’ll never buy beach homes for $370,000 again.

- I expect to start seeing a decline in pricing by the end of this year. It will be subtle at first but will pick up over the next year and the year after.

- Unlike the mortgage crisis last time, this cycle will be caused by UNAFFORDABILITY.

- Most importantly, the homes in this cycle are older, and many are not updated (many are over 20 years old). The condition will outweigh any other feature once the inventory spikes due to cost and inconvenience of remodeling out of state. See my previous blog about insurance requirements.

Let’s talk about unaffordability for a minute. This is not just an interest rate issue. In fact, even if interest rates come down to 5% again, it will only create a small impact on the overall cost of owning a beach home.

Consider this:

- Rising insurance costs. You can read the article in my newsletter about the recent rate increase request. While they have not historically gotten what they ask for, they’ve always gotten something. It’s already too expensive.

- Mortgage debt to income is stretched to 50% on conventional loans and 48% on Jumbo loans to qualify. That just means qualify. How sustainable is a 50% DTI long term?

- Car insurance is seeing the fastest rise it’s ever experienced, with an average 22% increase year over year.

- Utilities are rising.

- Construction/remodeling costs are the highest on record at over $300/sq ft.

- Rental occupancy is down 10%. While the rates are still elevated from the COVID years, that will quickly change if occupancy stays down.

- Real estate taxes are rising. Not so much here on the Outer Banks, but on your primary home in other states.

So, does this mean I’m saying it’s not a good time to buy? Not at all! It’s just not a good time for EVERYONE to buy. How so?

- If you are a LONG TERM investor, you will be fine. Even those who bought in 2005 at the peak made money in 2021 or 2022.

- Don’t buy anything that the rental income doesn’t at least cover the mortgage. Lowers your risk.

- If your DTI is at 40% or lower, your risk is very low and manageable.

- Real estate is a tangible asset. While the markets do fluctuate, they also never in history have gone to zero or even to the last cycle’s low.

However, if you are a current homeowner and your retirement plan includes the proceeds of this home, you may need to really consider how long you can/want to keep it. If you aren’t in to see this next cycle through, you have a prime time this spring to take advantage before what I believe is the end of this bull market.

Factor in the waning rental occupancy, rising costs, and the boomers knowing it’s time to cash out, it appears we will see an influx of inventory this spring. That will be the one catalyst to start a more rapid decline in pricing.

Please know that it’s never my intention to be a downer; I’m just a realist. You can’t avoid what you don’t see coming. It’s coming. I was taught that you can’t make the best decisions without looking at all the information. Please reach out if I can help you strategize your move in 2024.

November OBX Update

October 30, 2023 By Ilona

Let’s take a basic approach this month.

Here’s what we have:

Inventory is generally the highest in our spring market. This year, we are seeing a 26% increase in inventory in fall versus spring. That’s pretty unusual.

- Spring Average Inventory – 280 homes

- Fall Average Inventory – 380 homes

Similarly, sales are also at their highest in the spring market. Here, we see a normal 14% drop so far for fall.

- Spring 3-month average sold – 170

- Fall 3-month average sold – 145

It’s still not taking long to get properties sold.

- Median days on market is still pretty low at around 3 weeks.

Pricing hasn’t changed very much, despite seeing more price reductions. We aren’t seeing a tangible change just yet.

- Median price in spring vs fall is hovering right around $540,000

- 59% of closed properties sold UNDER asking price

- 22% sold AT asking price

- 19% sold MORE than asking price

While mortgage applications are down, it’s not impacting us yet.

- 30% of all sales in September were cash

Bottom line is for now, things are still moving along. However, there are these subtle differences. Markets don’t change all at once. It happens little, by little, by little, then all at once!

I’ll be watching.