With the latest news of the DC and Metro housing market, it is yet to be seen if or how that may trickle down to the OBX. A healthy percentage of our secondary homeowners live in that area. It would only take a 20% increase in our inventory, if buyer demand stays the same, to push us into a 9 month absorption rate. That would then put us on the verge of an unstable market. We need to keep a close eye on how this will affect us.

As for our latest stats, here’s what is happening:

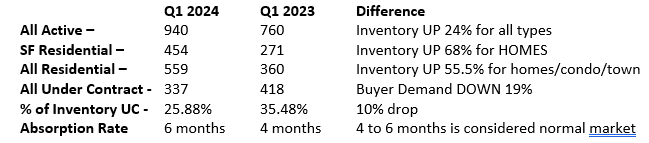

| Mid February 2025 | Mid February 2024 | |

| Active All | 1,153 | 889 |

| Active Houses | 586 | 411 |

| Under Contract | 287 | 331 |

| 3 Mo Sold Avg | 155 | 147 |

| Absorp Rate | 7.4 | 5.9 |

The numbers speak for themselves. Inventory is up, activity is down. We are seeing 75% of properties selling under list price. This is indicative of a normal market. We have only a small window of excess inventory before we enter “unstable” territory.

If you’re on the fence about selling, you might want to take a closer look.

In a nutshell, the market here is changing…slowly…but surely. These types of cycle shifts don’t happen all at once. Fortunately, because I study the market every day, I can help you see it coming. After all, you can get out of the way of what you don’t see!

In a nutshell, the market here is changing…slowly…but surely. These types of cycle shifts don’t happen all at once. Fortunately, because I study the market every day, I can help you see it coming. After all, you can get out of the way of what you don’t see! What a difference a year makes! Long story short, there are some BIG moves that are happening. I’ve talked before about algorithmic decay. This chart here is exactly that! Little, by little, by little, then bang. That’s how markets change. Tale as old as time, song as old as rhyme, it’s almost as good as a crystal ball.

What a difference a year makes! Long story short, there are some BIG moves that are happening. I’ve talked before about algorithmic decay. This chart here is exactly that! Little, by little, by little, then bang. That’s how markets change. Tale as old as time, song as old as rhyme, it’s almost as good as a crystal ball.

From what I have been told, there were many meetings amongst lots of organizations, Homebuilders Association and NC Realtors are included in the reshaping of the wastewater regulations. Negotiations were settled, the meeting concluded, and everyone went home. The night before the vote, the bill is sent out. Unbeknownst to all signings, changes were made in favor of the Septic Tank Association’s lobbyists, resulting in the incoming “shituation” we have now. This DID come from the private sector and the only way out of it is legislatively.

From what I have been told, there were many meetings amongst lots of organizations, Homebuilders Association and NC Realtors are included in the reshaping of the wastewater regulations. Negotiations were settled, the meeting concluded, and everyone went home. The night before the vote, the bill is sent out. Unbeknownst to all signings, changes were made in favor of the Septic Tank Association’s lobbyists, resulting in the incoming “shituation” we have now. This DID come from the private sector and the only way out of it is legislatively. With all the insurance and septic news, I’m going to be brief on this month’s market report and just give you the numbers straight up. With only one month in, there isn’t a lot to analyze anyway.

With all the insurance and septic news, I’m going to be brief on this month’s market report and just give you the numbers straight up. With only one month in, there isn’t a lot to analyze anyway. History repeats itself. A saying I’m sure you’ve heard and said dozens of times. I might not yet be a half of a century old, but I’m old enough, and have been in this business long enough (27 years) to recognize a similar pattern. Let’s revisit the timeline of the Outer Banks real estate market from the year 2000.

History repeats itself. A saying I’m sure you’ve heard and said dozens of times. I might not yet be a half of a century old, but I’m old enough, and have been in this business long enough (27 years) to recognize a similar pattern. Let’s revisit the timeline of the Outer Banks real estate market from the year 2000.